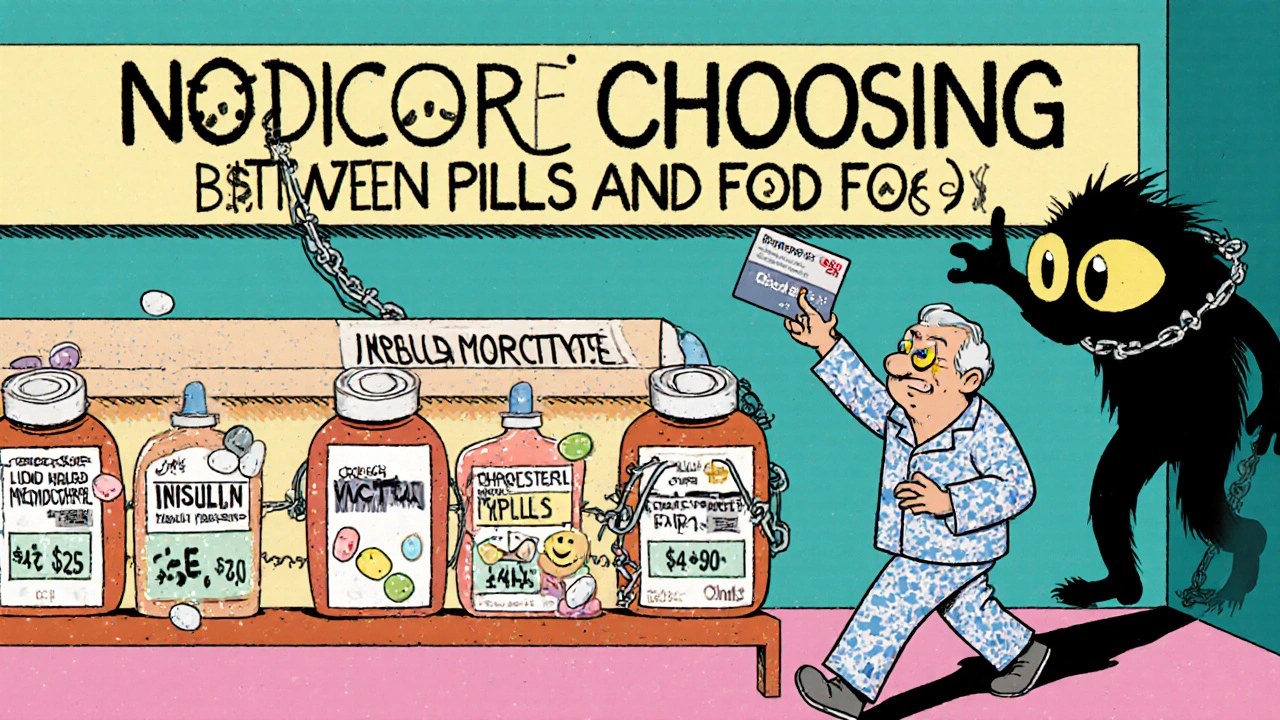

For many seniors on Medicare, the cost of daily medications can be a crushing burden. A single generic prescription for blood pressure, cholesterol, or diabetes can cost $30, $50, even $100 a month without help. But if you qualify, Medicare Extra Help can cut those costs to as little as $1.60 per pill - and eliminate your monthly premium and deductible entirely. This isn’t a theoretical discount. It’s real, life-changing savings that thousands of people use every day to stay healthy.

What Medicare Extra Help Actually Covers

Medicare Extra Help, officially called the Part D Low-Income Subsidy (LIS), is a federal program designed to help people with limited income and resources pay for their prescription drugs. It doesn’t just reduce copays - it removes almost all out-of-pocket costs for Part D coverage. In 2025, if you qualify, you pay $0 for your Part D plan premium and $0 for your deductible. For generic drugs, you pay no more than $4.90 per prescription. If your income is below 100% of the Federal Poverty Level and you also get Medicaid, your copay drops to just $1.60.

Compare that to standard Medicare Part D. Without Extra Help, you’d pay up to $595 just to start getting coverage. Then, for a $50 generic drug, you’d pay 25% - $12.50 - after that deductible. Multiply that by 12 prescriptions a month, and you’re paying nearly $750 a year just in copays, not counting the premium. With Extra Help? $705.60 total for the year - and you never paid the $595 deductible. That’s $1,345 saved in one year, just on generics.

Who Qualifies for Extra Help in 2025

Eligibility is based on strict income and resource limits. For 2025, an individual must earn less than $23,475 per year. For a married couple living together, the limit is $31,725. These numbers include Social Security, pensions, wages, and other income - but not housing assistance, food stamps, or medical care payments.

Resources matter too. You can’t have more than $17,600 in countable assets if you’re single, or $35,130 if you’re married. This includes bank accounts, stocks, bonds, mutual funds, and IRAs. Your primary home, one car, and personal belongings don’t count. You’re also allowed $1,500 per person for burial expenses without it affecting your eligibility.

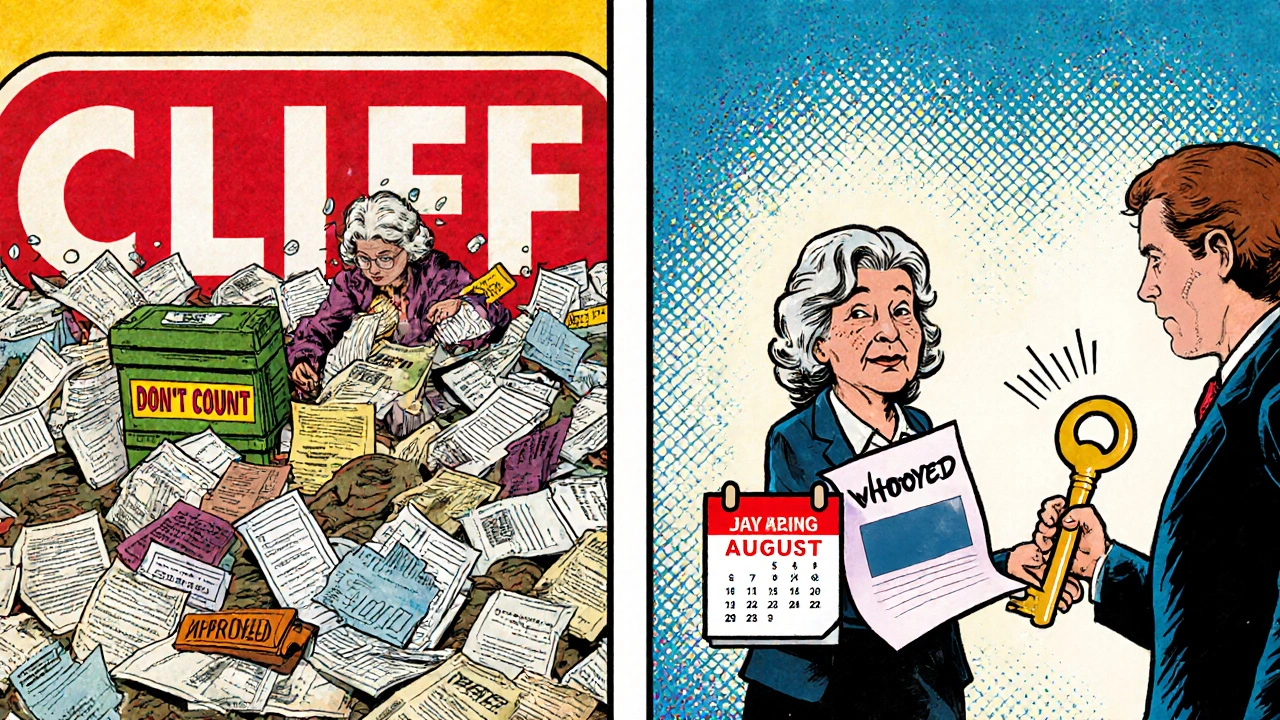

Here’s the catch: if you’re just $500 over the income limit, you lose everything. No partial help. No sliding scale. That’s why so many people who struggle to pay for meds still don’t qualify. A 78-year-old woman living on $24,000 a year from Social Security and a small pension might be paying $1,200 a year for her three generics - and she doesn’t qualify for Extra Help. That’s the cliff effect experts warn about.

How to Apply - And Why Most People Don’t

You can apply for Extra Help in three ways: online at SSA.gov, by calling 1-800-772-1213, or in person at your local Social Security office. If you already get Supplemental Security Income (SSI), Medicaid, or a Medicare Savings Program, you’re automatically enrolled. No paperwork needed.

But here’s the problem: according to the Medicare Rights Center, 37% of people who qualify never enroll. Why? The application is confusing. It asks for detailed financial records - bank statements, investment accounts, tax forms - that many seniors don’t have handy. One woman in Ohio spent three months trying to gather documents after her husband passed away. She finally got help from her local SHIP (State Health Insurance Assistance Program) and got approved - but she’d already skipped her heart medication for two months.

Don’t try to do this alone. Call your local SHIP. They’re free, trained, and available in every state. They’ll walk you through the form, help you gather documents, and even call Social Security on your behalf. In 2024, 73% of applicants needed this kind of help to complete the process.

What Happens After You’re Approved

Once approved, your Extra Help kicks in automatically with your Part D plan. You’ll see the lower copays at the pharmacy counter - no extra card, no coupon, no registration. Just show your Medicare card. Your plan will know you’re enrolled.

You also get a special enrollment period. Normally, you can only switch Part D plans once a year during Open Enrollment. But with Extra Help, you can change plans once a month. That’s huge. If your favorite generic gets pulled from your plan’s formulary, or your pharmacy stops participating, you can switch to a better plan without waiting.

Every August, you’ll get a form in the mail asking you to update your income and resources for next year. You have 30 days to return it. If you don’t? Your Extra Help ends on January 1. No warning. No grace period. Just a sudden jump in your monthly drug costs. That’s why so many people lose it - not because they earned too much, but because they missed a deadline.

Real Stories - The Good, The Bad, The Ugly

One man in Florida, 82, takes five generic drugs for diabetes, high blood pressure, and arthritis. Before Extra Help, he was spending $2,100 a year on meds. After approval? $59 a year. He said, “I finally stopped choosing between my pills and my groceries.”

Another woman in California, 76, got her Social Security increase in January. Her income went from $23,200 to $23,700 - just $500 over the limit. She lost Extra Help. Her copays jumped from $4.90 to $35 per prescription. She now pays $1,200 a year for three meds. She says, “I’m not rich. I’m just one paycheck away from being ineligible.”

These aren’t rare cases. The Medicare Payment Advisory Commission found that Extra Help beneficiaries are 23 percentage points more likely to take their meds as prescribed than those without it. That’s not just about money - it’s about survival. Skipping insulin or blood pressure meds leads to hospitalizations, which cost Medicare far more than the subsidy ever does.

What’s Changing in 2025 and Beyond

This year, the Part D “donut hole” - that gap in coverage where you pay full price - no longer exists for Extra Help recipients. You get full coverage all year. That’s a big win.

Also in 2025, insulin is capped at $35 per month for all Medicare Part D beneficiaries. That means even if you don’t qualify for Extra Help, your insulin won’t cost more than that. But for those who do qualify, it’s just one more layer of protection.

There’s talk in Washington about expanding eligibility to people earning up to 175% of the Federal Poverty Level - that would raise the income limit to about $28,500 for an individual. If that happens, over a million more seniors could get help. But for now, the rules stay the same.

What to Do Next

If you or someone you care about is on Medicare and paying more than $10 a month for generic prescriptions, you should check your eligibility. Don’t assume you make too much. The limits are low, but many people don’t realize what counts as income or resources.

Step one: Call 1-800-MEDICARE (1-800-633-4227) and ask about Extra Help. They’ll send you an application.

Step two: Contact your local SHIP. Find them at shiptacenter.org. They’ll help you fill out the form, explain what documents you need, and even check if you qualify for other state programs.

Step three: Don’t wait. Apply now. The process takes 3 to 6 weeks. If you wait until December, you might lose your savings for the whole next year.

Medicare Extra Help isn’t a luxury. For millions of seniors, it’s the difference between staying healthy and going without. It’s simple, direct, and life-saving. If you qualify - and many more people do than think - don’t let bureaucracy keep you from what you’re owed.

Do I have to reapply for Extra Help every year?

No, you don’t have to reapply from scratch. But every August, you’ll get a form in the mail asking you to update your income and resources for the next year. You must return it within 30 days. If you don’t, your Extra Help ends automatically on January 1. Many people lose benefits not because they earned too much, but because they missed this annual review.

Can I still get Extra Help if I have savings in a bank account?

Yes - as long as your total countable resources don’t exceed $17,600 for an individual or $35,130 for a married couple in 2025. Your primary home, one car, personal belongings, and up to $1,500 per person for burial expenses don’t count. But bank accounts, stocks, bonds, mutual funds, and IRAs do. If you’re unsure what counts, contact your local SHIP for a free review.

What if my income goes up a little and I lose Extra Help?

Losing Extra Help because of a small income increase is common - and devastating. If your Social Security cost-of-living adjustment pushes you over the limit, you’ll suddenly pay full Part D premiums and copays. You can’t appeal the loss, but you can reapply if your income drops again. Some people delay taking raises or switch to lower-cost meds to stay eligible. The system doesn’t offer a buffer, so plan ahead.

Can I use Extra Help with any Part D plan?

Yes - but you still need to choose a plan. Extra Help doesn’t come with a plan of its own. You must enroll in a Medicare Part D plan that accepts the subsidy. All standard plans do. The program doesn’t restrict which plans you can join. In fact, you can change plans once a month if your current one doesn’t cover your meds well or has a bad pharmacy network.

Are brand-name drugs covered under Extra Help?

Yes. Extra Help covers both generic and brand-name drugs. For brand-name prescriptions, you pay up to $12.15 in 2025 - still far less than the full price. But because generics are usually cheaper and just as effective, most people on Extra Help use them. If your doctor prescribes a brand-name drug, your plan may require prior authorization - but Extra Help beneficiaries can request formulary exceptions more easily than others.

Reviews

Let’s deconstruct the epistemological framework of pharmaceutical access under Medicare Part D. The structural violence inherent in the $500 income cliff isn’t merely a policy failure-it’s a neoliberal artifact that reifies biopolitical control over aging bodies. The LIS program, while ostensibly benevolent, operates as a gatekeeping mechanism that pathologizes poverty while refusing to dismantle the capitalist architecture that renders medication a commodity rather than a human right. The fact that 37% of eligible individuals remain unenrolled isn’t a failure of outreach-it’s a feature of a system designed to exclude the very people it purports to help.

Oh please. Another ‘poor elderly’ sob story. I mean, come on. If you can’t afford your meds, maybe you shouldn’t have spent your entire life on Netflix and takeout. I’m not saying people shouldn’t get help-but why should I, a 32-year-old who works two jobs, subsidize someone who didn’t plan for retirement? Also, ‘$1.60 per pill’? That’s not saving, that’s a handout wrapped in virtue signaling. 🤦♂️

I’m curious-when the form asks for bank statements, does it include joint accounts with adult children? My mom’s got a joint savings account with my brother, and she’s terrified that even though the money’s mostly his, it’ll disqualify her. I’ve been trying to find a clear answer, but every source says something different. Anybody know how they treat those?

Important note: if you're applying online, make sure you have your Social Security number, bank account info, and a list of all your prescriptions ready. Also-don’t panic if you’re just over the income limit. Sometimes, if you have high medical expenses, you can appeal. Call SHIP. They’ve helped me with three family members. No charge. No hassle. Just real people who know the system. And yes, burial funds are exempt-so don’t worry about that $2,000 you set aside for funeral costs. 🙏

Let me be perfectly clear: this program is not a privilege-it is a moral imperative. The fact that seniors are forced to choose between insulin and groceries in the wealthiest nation on earth is not just tragic-it is a national disgrace. The $500 income cliff is not a policy-it is a cruel joke. And yet, we celebrate it as ‘fiscal responsibility.’ We call it ‘targeted assistance’ when what we’re really doing is punishing people for living too long, too poor, and too sick. We need systemic reform-not more paperwork. We need universal coverage-not a patchwork of eligibility thresholds that leave millions hanging by a thread. This isn’t about Medicare. This is about dignity.

Just wanted to add-many people don’t realize that if you’re on Medicaid, you’re already enrolled in Extra Help. No application needed. If you’re not sure, check your Medicaid card or call your state’s Medicaid office. Also, if you’re approved, your pharmacy will automatically apply the discount-you don’t need a card or code. Just show your Medicare card. I’ve seen too many people panic and pay full price because they thought they needed to ‘activate’ it. You don’t. It’s already done.

Bro, this is wild. I’m from Nigeria, and we don’t even have this kind of system. Here, if you can’t pay, you don’t get the med. Period. So I’m like… why is America still making this so hard? 😅 You got the money, you got the infrastructure, you got the tech… why the hell is this so complicated? I just want to see grandma get her pills without crying over paperwork. 🤷♂️

Another socialist handout disguised as compassion. Let me guess-next they’ll give us free housing and food stamps for the ‘deserving poor.’ This isn’t help, it’s dependency. If you can’t afford your meds, maybe you shouldn’t have retired at 62. Or maybe you shouldn’t have bought that $400 TV. The government shouldn’t be your financial advisor. Stop rewarding poor life choices with taxpayer money. 🇺🇸

My dad got approved last year. Pays $1.60 for his blood pressure med. Used to pay $45. He cried when he found out. Didn’t say much. Just nodded. That’s all you need to know.